4. Portfolio Diversification and Supporting Financial Institutions (CAPM Model)

Financial Markets (ECON 252)

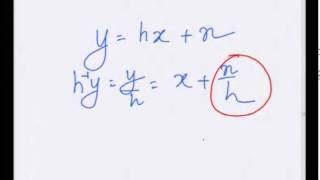

Portfolio diversification is the most fundamental concept of risk management. The allocation of financial resources in stocks, bonds, riskless, assets, oil and other assets determine the expected return and risk of a portfolio. Taking account of covariances and expected returns, investors can create a diversified portfolio that maximizes expected return for a given level of risk. An important mission of financial institutions is to provide portfolio-diversification services.

00:00 - Chapter 1. Introduction

02:37 - Chapter 2. Evaluation of Efficient Portfolio Frontiers

26:59 - Chapter 3. The Significance of Portfolio Diversification

38:43 - Chapter 4. The Tangency Portfolio and the Mutual Fund Theory

51:46 - Chapter 5. The Capital Asset Pricing Model

59:09 - Chapter 6. Implications of the Equity Premium and Conclusion

Complete course materials are available at the Open Yale Courses website: http://open.yale.edu/courses

This course was recorded in Spring 2008.